TSM and MU strength versus NVDA weakness points to a more selective AI trade.

The AI theme is not broken. Capital is rotating away from the most crowded single GPU leader and toward memory, foundry, advanced packaging and supply-chain bottlenecks that can still show earnings certainty.

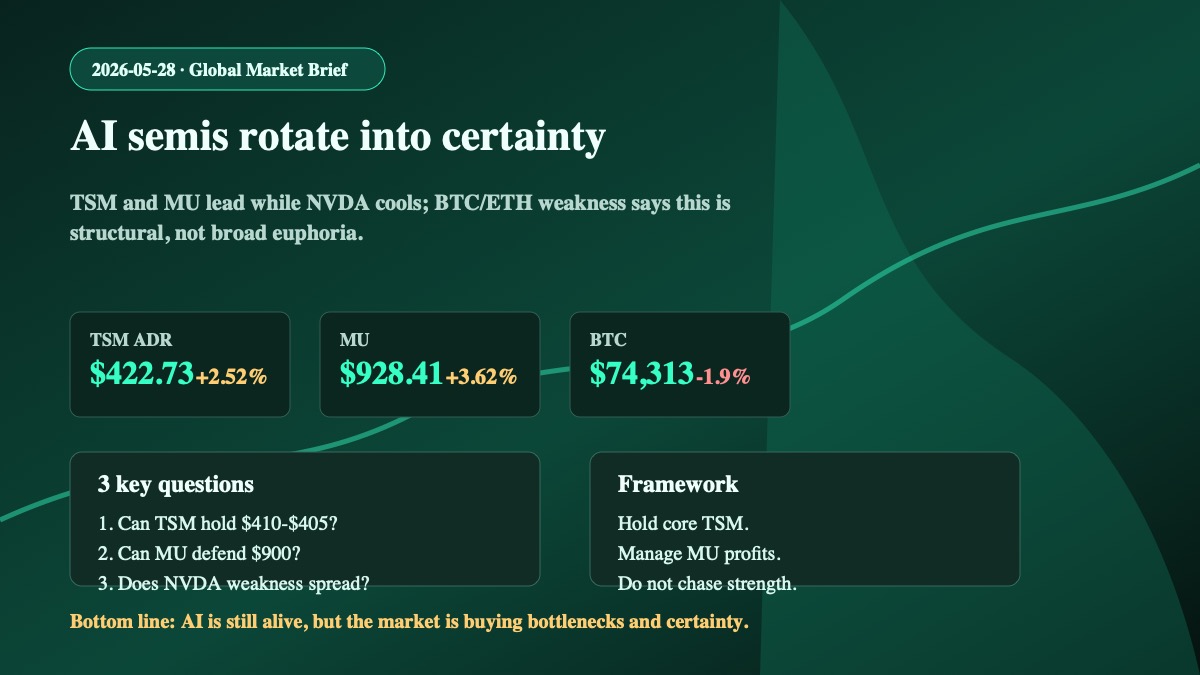

1. TSM and MU are the signalTSM ADR rose 2.52% to $422.73 and MU rose 3.62% to $928.41, while NVDA fell about 0.91% to $212.90. This is internal AI semiconductor rotation, not a broad index move.

2. Taiwan confirms the directionTaiwan Weighted traded near 44,641.39, up about 0.87%, while TSM 2330.TW traded near NT$2340, up about 1.74%, with an intraday high near NT$2360.

3. Crypto is not confirming a full risk-on moveBTC was near 74,313 and ETH near 2,019, both weaker versus prior references. AI semis are strong because of industry logic, not simply because cross-asset risk appetite is euphoric.

4. Plain-English takeawayTSM still fits a core AI infrastructure role. MU remains a high-beta profit-management trade after a strong move, with $900, $880 and $860 as useful risk markers.