MU is the strongest HBM signal, while TSM remains the core AI infrastructure holding.

The AI capex thesis is intact, but the trade is more selective. TSM is still a core position; MU has moved from entry logic into active profit-management territory after rising from $810 to $971.

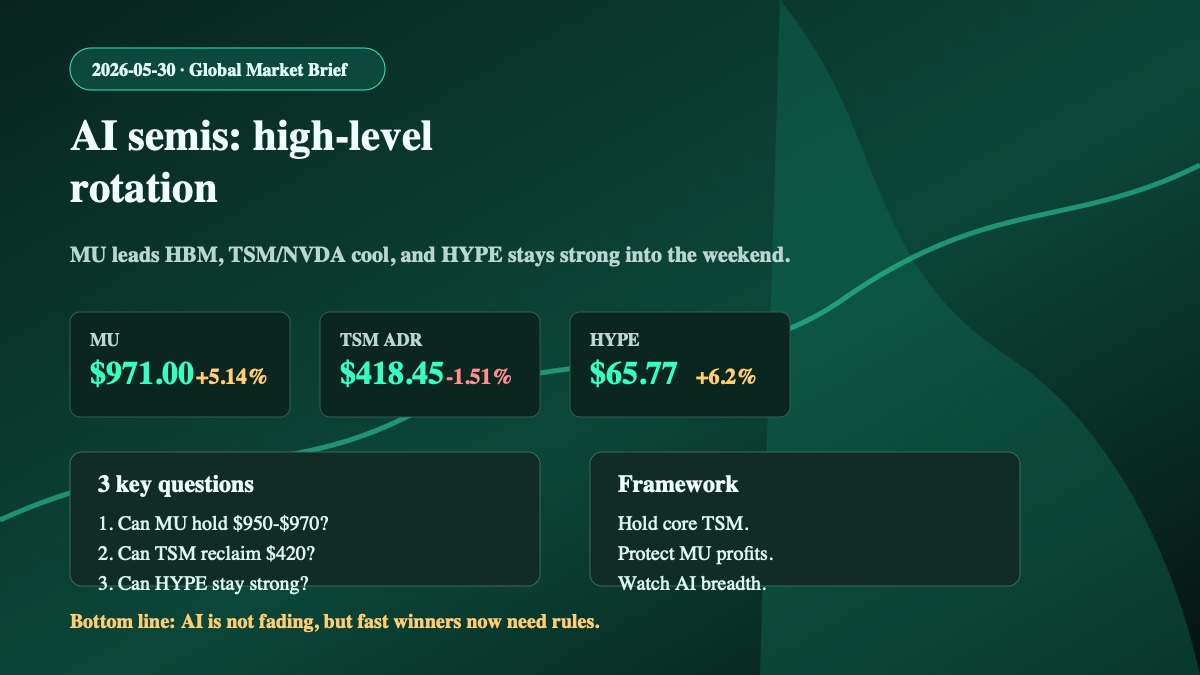

1. MU leads the HBM tradeMU closed at $971.00, up about 5.14%, after touching $981. The move confirms strong memory/HBM demand, but nearly 20% profit from the $810 entry needs protection.

2. TSM and NVDA pull back, not breakTSM ADR fell about 1.51% to $418.45 and NVDA fell about 1.45% to $211.14. With QQQ and SPY still higher, this looks like profit rotation rather than AI-theme failure.

3. Taiwan still confirms TSMTaiwan 2330.TW closed at NT$2355, up about 2.61%, with high volume. As long as NT$2300 holds, the core TSM thesis remains constructive.

4. HYPE remains a positive weekend signalHYPE traded near $65.77, up about 6.2%, while BTC and ETH were broadly stable. Hyperliquid risk sentiment remains firm rather than stressed.