TSM stays core, MU needs profit rules, and HYPE remains the strongest crypto signal.

The AI semiconductor trend is intact. Taiwan’s TSM strength matters more than one ADR pullback, while MU’s fast move toward $1000 requires a written profit-protection plan.

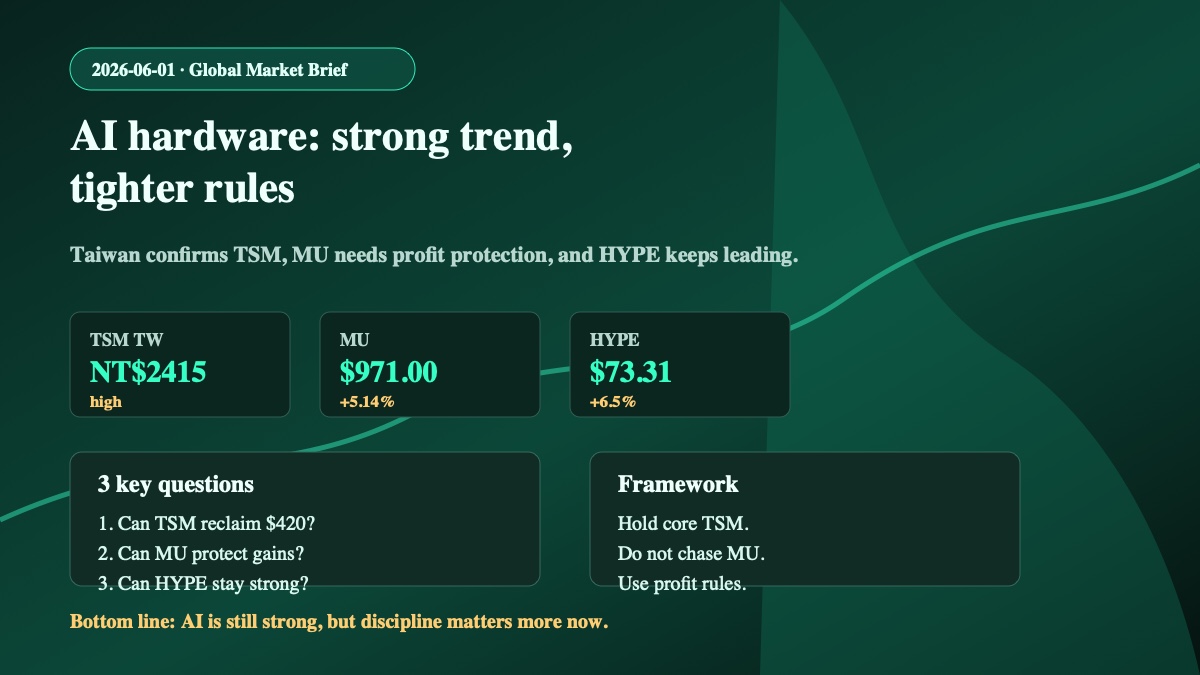

1. Taiwan confirms TSMTaiwan Weighted traded near 45,419, up about 1.53%, while 2330.TW reached NT$2415 intraday. As long as NT$2350-2300 holds, the TSM core thesis remains constructive.

2. MU is now a profit-management tradeMU closed at $971.00 on Friday, up about 5.14%, and the $810 entry now shows about 19.9% unrealized profit. The trade is strong, but the next job is protecting gains.

3. NVDA pullback is not AI capex failureNVDA fell about 1.45% on heavy volume, but Nvidia’s FY2027 Q1 revenue and data-center growth still support the AI factory demand thesis.

4. HYPE leads Hyperliquid sentimentHYPE traded near $73.31, up about 6.5%, while BTC/ETH were slightly weaker. That is not a broad crypto risk collapse; HYPE remains the standout signal.